No Exit, No Party

Let me be clear from the start:

-

No, this article is not about your startup - you'll raise capital and have a 10X exit

-

No, this article is not about you as an investor - all your portfolio will have successful IPOs

What this is, however, is an honest look at the market data and the current situation we're all navigating together. And yes, I do believe things will change, the numbers and dynamics we're seeing today won't last forever.

The financial markets are experiencing a perfect storm that's creating unprecedented challenges across the entire investment ecosystem. What started as elevated interest rates and geopolitical uncertainty has evolved into a fundamental bottleneck, choking off traditional exit strategies and creating ripple effects throughout venture capital and private equity.

While we've witnessed a few high-profile successful exits recently, particularly in the fintech sector - these exceptional deals shouldn't mask the broader reality facing most companies and investors. For the vast majority, the message is becoming clear: traditional paths to liquidity have become significantly more challenging, and the alternatives are facing their own constraints. However, while the current environment presents significant challenges, there are emerging solutions and adaptations that offer reasons for cautious optimism that we'll explore as potential paths forward.

The IPO Window Has Been Closed For A While

The public markets have become incredibly selective, with only the most established companies managing successful offerings. We're seeing IPO volumes at multi-year lows, and the few companies brave enough to attempt public offerings face an increasingly challenging environment.

This selectivity has created an enormous backlog. Companies that would traditionally have gone public after 7-10 years are now extending their private market tenure indefinitely, waiting for conditions to improve. The result is a growing queue of mature, venture-backed companies competing for the attention of increasingly cautious public investors.

For most companies, going public simply isn't a viable option right now. The market has become an exclusive club where only giants with bulletproof financials and exceptional growth metrics can succeed.

M&A Markets Face Their Own Crisis

With IPOs off the table, mergers and acquisitions should theoretically be booming as the primary exit mechanism. Instead, the M&A market is dealing with its own set of serious constraints that are severely limiting deal activity.

Market sentiment tells the story. The BCG M&A Sentiment Index shows decision makers have grown increasingly pessimistic, with the current reading of 74, indicating expectations for below-average activity over the next six months.

Several factors are driving this decline. Higher interest rates have made debt financing more expensive, reducing the attractiveness of leveraged buyouts. Ongoing geopolitical tensions and trade uncertainties have made corporate boards more risk-averse. The Trump administration's tariff policies have added complexity around cross-border transactions and international expansion strategies.

The numbers are stark: deal signing activity has fallen to 20-year lows, reaching levels worse than during the 2008 financial crisis. Even the pandemic didn't hit M&A activity this hard.

Private Equity's Liquidity Constraints

Private equity firms, traditionally major drivers of M&A activity, are facing their own capital constraints. The scope of the problem becomes clear when looking at portfolio company volumes: PE firms are currently holding nearly 30,000 companies globally that they're waiting to sell.

The core issue lies in the relationship between available capital and existing obligations. The ratio of dry powder (un-invested capital) to unrealized value (the paper value of portfolio companies that haven't been sold yet) has fallen to its lowest level in 25 years. This metric is crucial because it represents the actual purchasing power of PE firms relative to their existing commitments.

When this ratio is low, PE firms have less available capital to deploy on new acquisitions relative to the value tied up in existing investments. With portfolio companies taking longer to exit, these firms are effectively capital-constrained despite having raised significant amounts in previous years.

This dynamic has reduced the number of active buyers in the M&A market. Private equity firms that once competed aggressively for attractive assets are now being more selective and conservative, resulting in fewer bidders, longer sales processes, and downward pressure on valuations.

The Fundraising Cascade Effect

The exit market paralysis is creating significant downstream effects in fundraising. Venture capital and private equity funds return capital to limited partner investors through exits, either IPOs or M&A transactions. When exits stall, funds can't distribute returns, directly impacting their ability to raise subsequent funds.

The scale of the challenge becomes clear when examining the sheer volume of venture-backed companies awaiting liquidity. The number of VC-backed companies has exploded from roughly 10,000 in 2010 to nearly 60,000 by 2024, while the number of publicly listed domestic companies on major US exchanges has remained essentially flat at around 4,000. This massive divergence illustrates why the US public market simply cannot absorb the disproportionately large inventory of private companies waiting to go public.

Limited partners, facing their own liquidity constraints and uncertainty about return timelines, have become increasingly selective about new fund commitments. This has extended typical fundraising cycles and made it significantly more challenging for investment managers to secure capital for new vehicles.

The result is a funding ecosystem operating under much tighter constraints than the previous decade's capital abundance.

Startup Funding Requirements Escalate

The impact on startup funding has been measurable and dramatic. Funding cycles have extended from an average of two years to three years, forcing companies to manage cash more carefully and extend their runways considerably.

More concerning for entrepreneurs, the performance thresholds required to secure funding have risen substantially. Where startups previously needed to demonstrate $1 million in annual recurring revenue to raise a Series A, that benchmark has increased to $3 million or more in many cases.

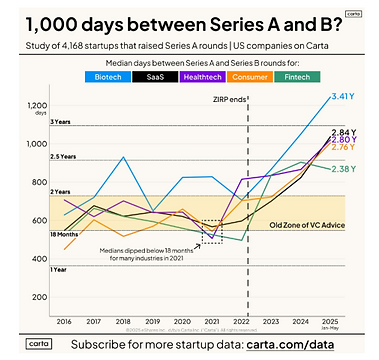

The time between funding rounds has also extended significantly. The median time between Series A and Series B rounds now approaches 1,000 days (nearly three years), representing a fundamental shift from the 18-24 month cycles that were standard during previous years.

Investors are demanding more than just growth, they want sustainable unit economics, clear paths to profitability, and more conservative growth projections. The era of growth-at-all-costs has definitively ended, replaced by a focus on building fundamentally sound business models.

Market Implications and Structural Changes

This environment represents a fundamental shift from the capital abundance of the previous decade. Companies that raised money expecting relatively easy access to follow-on funding are discovering a much more challenging landscape. Some are being forced to accept down rounds or structured deals that would have been unthinkable just a few years ago.

The crisis is forcing the venture capital industry to reinvent itself. Traditional VC funds face regulatory restrictions that limit them to private companies and 10-year fund lifecycles. With companies staying private longer and exits becoming scarce, these constraints have become problematic.

Major funds like Sequoia, Andreessen Horowitz, and General Catalyst are now registering as Registered Investment Advisors (RIAs), which removes these restrictions. This allows them to invest in public stocks, buy stakes from other funds, acquire controlling interests, and hold investments indefinitely. Some are also adopting "evergreen" structures without fixed end dates, eliminating pressure to exit when fund terms expire.

For companies that successfully navigate this environment, there are potential advantages. Reduced competition for talent, lower marketing costs, and more rational pricing create opportunities for efficient operators to build strong market positions.

However, the overall ecosystem contraction means many promising companies may not survive long enough to see improved market conditions. The current environment is particularly challenging for capital-intensive businesses or those requiring sustained investment before reaching profitability.

Looking Ahead

Resolving this liquidity crisis will likely require improvement across multiple fronts: interest rate normalization, reduced geopolitical tensions, and most importantly, successful exits that allow capital to flow back to investors.

One trend that's gaining momentum as a potential solution is companies choosing to sell earlier in their lifecycle rather than waiting for traditional exit windows. For companies, this provides much-needed liquidity without having to meet increasingly high IPO bars or wait for the M&A market to fully recover. For acquirers, buying companies earlier typically requires less capital while reducing execution risk, allowing them to purchase proven business models at more reasonable valuations.

The companies and funds that adapt to this reality - building sustainable business models, managing capital efficiently, and considering earlier exit opportunities will be best positioned when market conditions eventually improve. For now, with no easy exits available, there's no party in sight. The question isn't whether conditions will improve, but when and which players will still be standing when they do.